Option prices and their impact on derived analytics

Frank Ferstler, Nicholas Pezolano

2022-12-12

Unlike with equities, option prices do not have an official NBBO closing price, this has been well studied in the context of option trading, however in this post we explore the impact on signals for equities. Most option trading systems will attempt to close their books by 1-5 minutes before the closing price. Using “live” trading bid ask spreads a minute before the close can provide more accurate trading prices. When using option derived analytics as equity signals which option price is preferred? As an example consider the most active strike and maturity for the SPY on 2020-12-30 and a less active strike/maturity.

Data for a SPY 373 Strike Call expiring on 2020-12-31

|

Time |

Underlying Price |

Bid |

Mid |

Ask |

Volume |

|

3:59 pm |

371.99 |

0.09 |

0.095 |

0.1 |

237672 |

|

4.00 pm |

372.03 |

0.2 |

0.235 |

0.27 |

248287 |

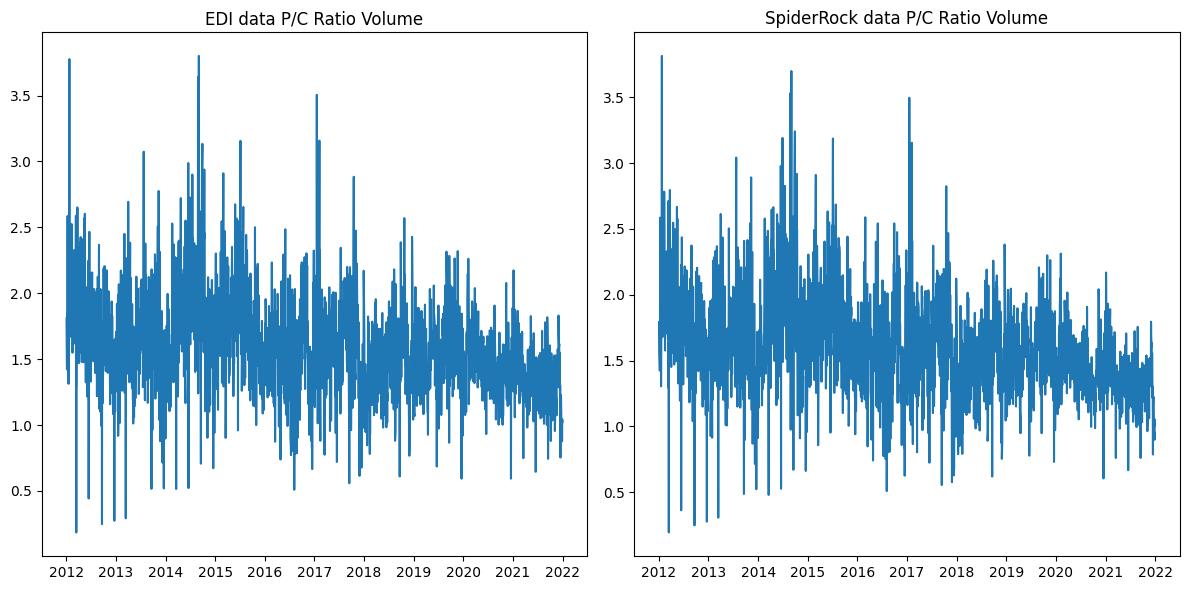

We consider two commonly explored options-implied equity signals, the Put-Call Volume Ratio in percentage terms and the IV Spread. The P/C Ratios at first glance look very similar.

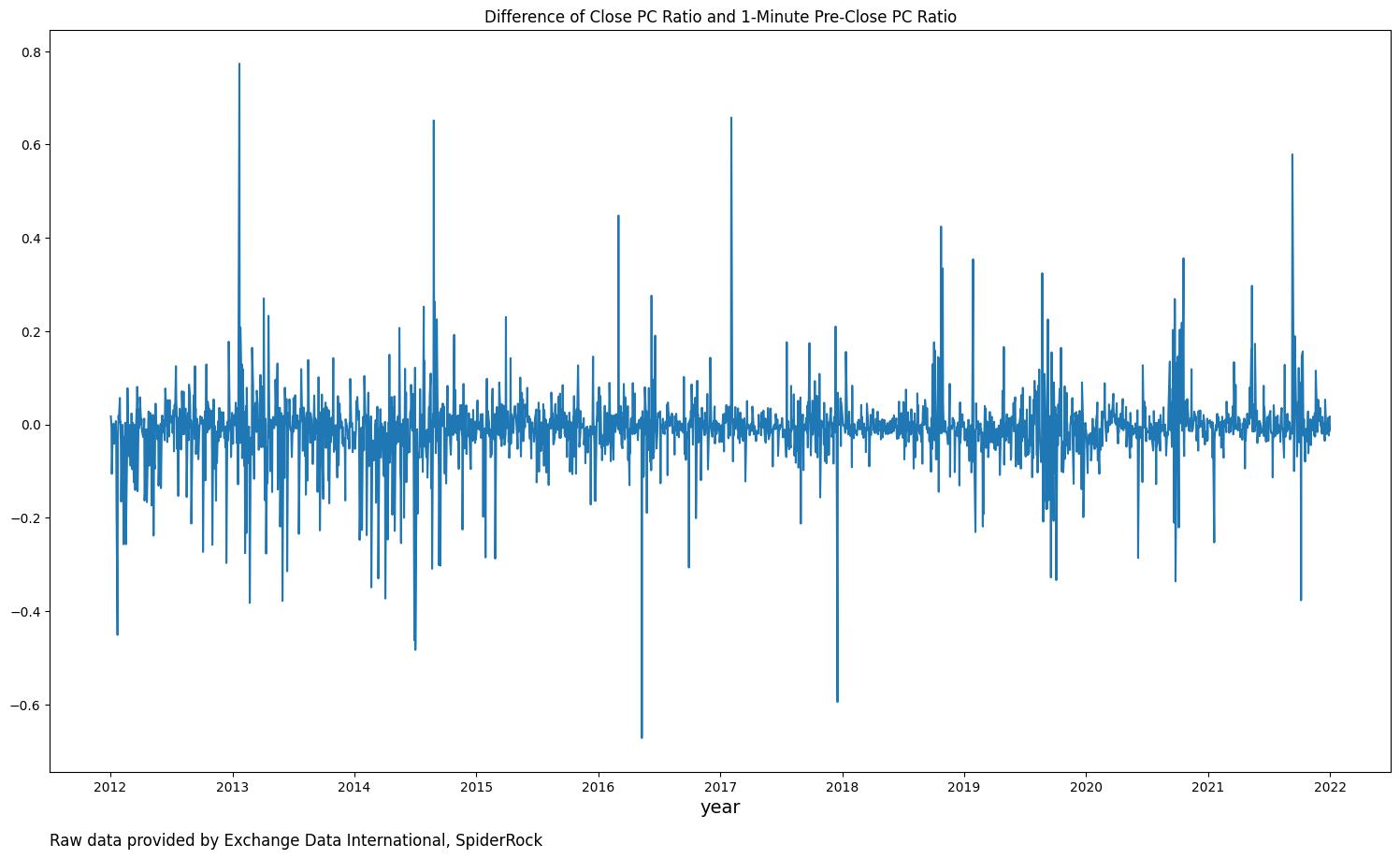

However when looking at the differences this shows there is reason to consider the impact both data sources can have when generating equity signals.

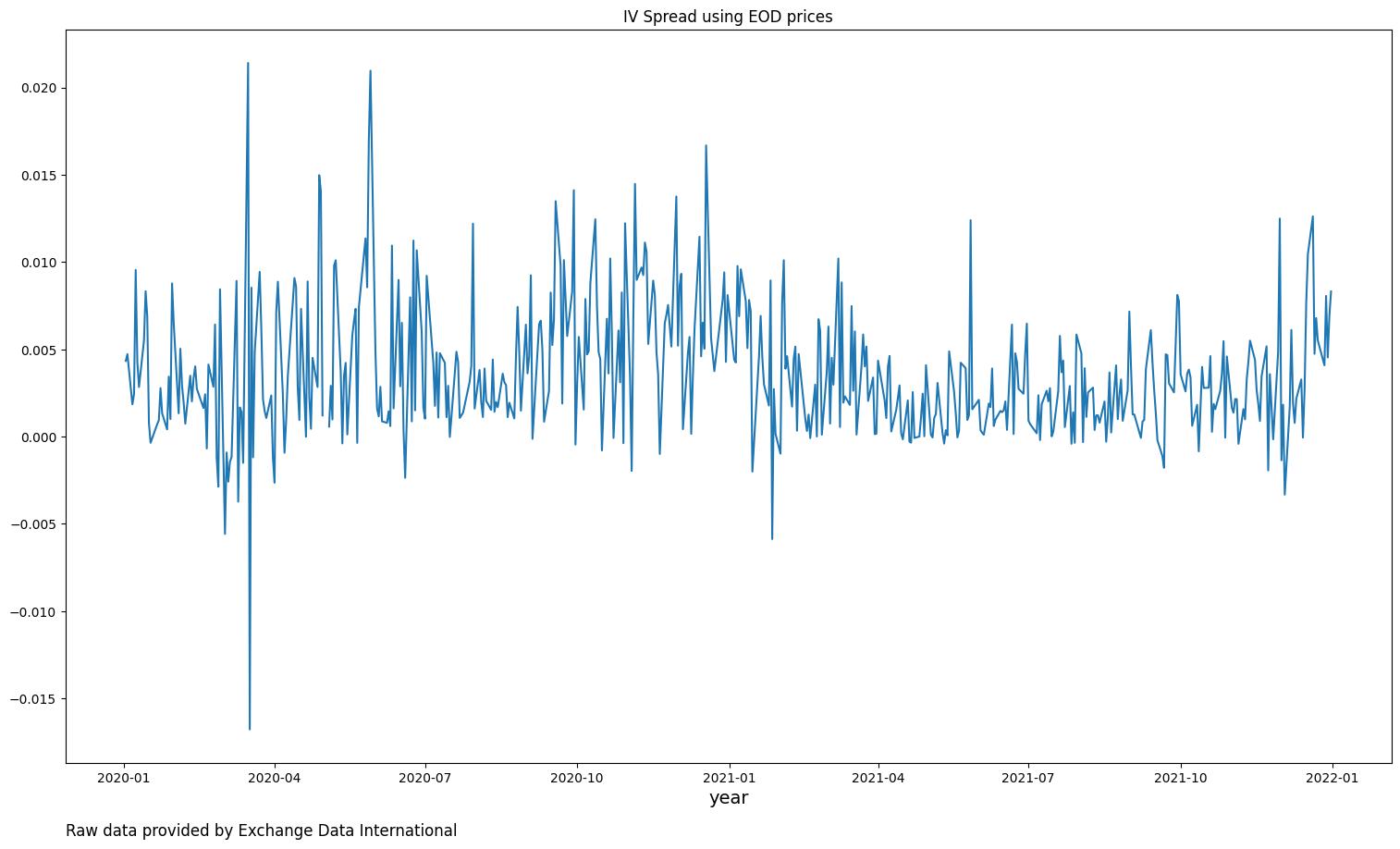

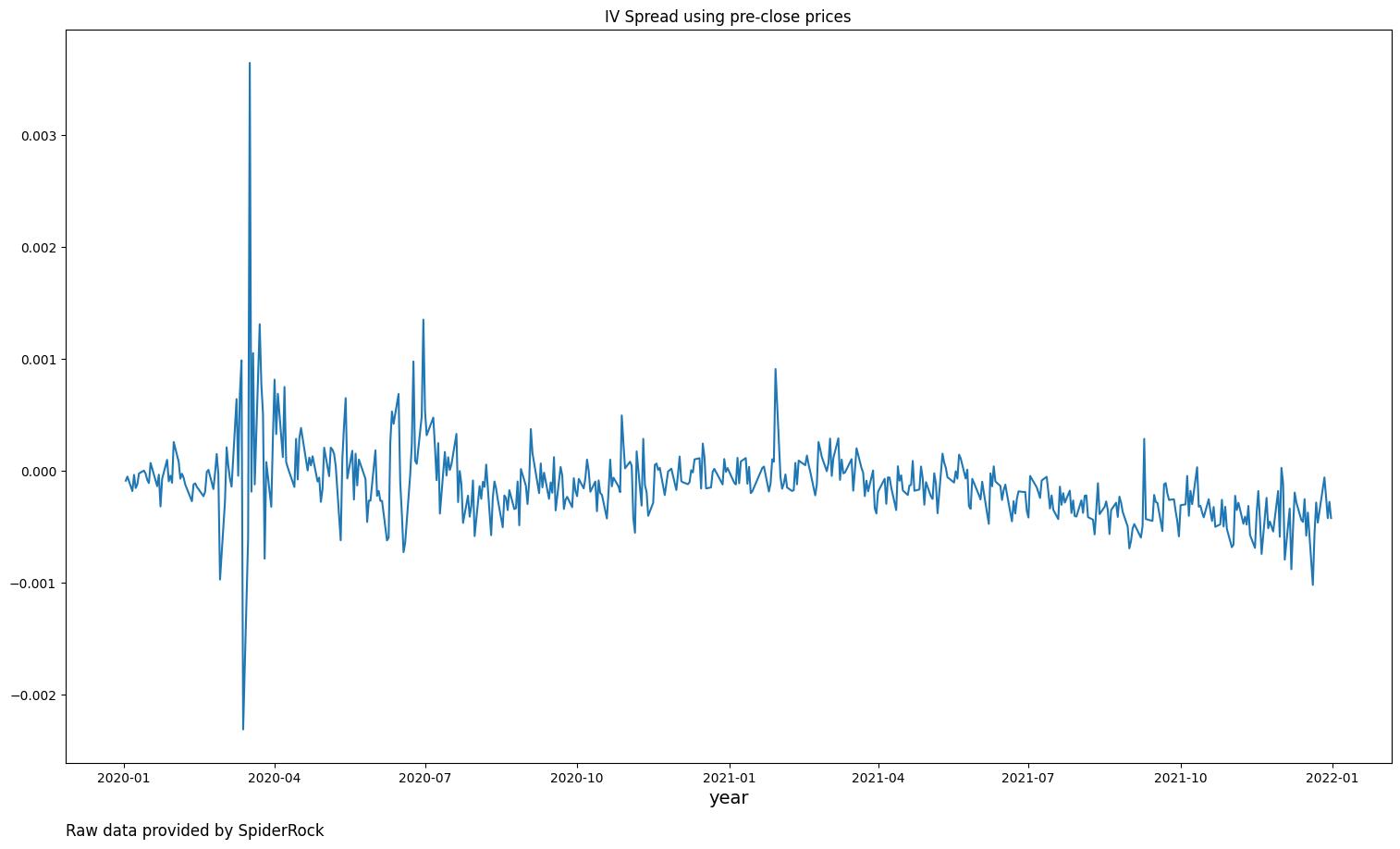

We also consider the impact these prices can have on Implied Volatility derived signals. IV derived signals using the pre-close prices provide a smoother signal that may be useful for certain applications or models that require a smoother signal.

Newmark Risk's goal is to provide high quality analytics to equity portfolio managers, to achieve this goal we rely on high quality input data sets from trusted data vendors such as Exchange Data International or SpiderRock, who each adds value in their own way.